Hard screening metrics — BWAY (TTM through March 31, 2026)

Market cap and OCF clear filters cleanly. TTM revenue growth straddles 30% depending on data source — see Caveat 1. PEG is Finviz single-source — see Caveat 2.

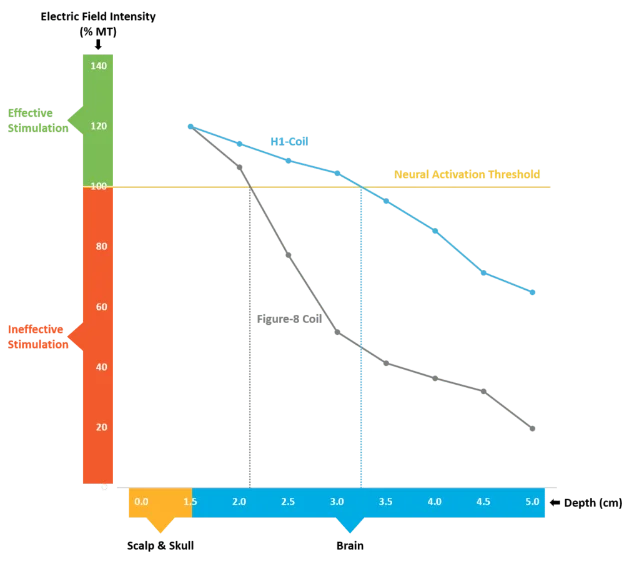

BrainsWay (BWAY) is Pass #23 — the series' first neuromodulation pick. $593M cap, TTM revenue ~30%, PEG 0.89 (single-source), OCF +$13.7M. Three FDA indications, Cigna prior-auth gone.

| Filter | Threshold | Reported value | Source(s) | Status |

|---|---|---|---|---|

| Market cap | < $10B | $593M | Finviz, StockAnalysis | ✅ Pass |

| TTM revenue growth | > 30% | 30.18% (Finviz) / 29.37% (StockAnalysis) | Finviz, StockAnalysis | ⚠️ Borderline |

| PEG ratio | < 1.0 | 0.89 (P/E 65.40 ÷ 5Y EPS growth 46.85%) | Finviz only | ✅ Pass (single-source) |

| Operating cash flow | Positive | +$13.65M–$14.18M TTM | StockAnalysis | ✅ Pass |

| Input | Value | Source |

|---|---|---|

| Trailing P/E | 65.40× (Finviz) / 67.72× (StockAnalysis) | Finviz / StockAnalysis |

| Forward P/E | 41.60× (Finviz) / 42.52× (StockAnalysis) | Finviz / StockAnalysis |

| EPS 5-year growth estimate | 46.85% | Finviz |

| PEG (Finviz method) | 0.89 | Trailing P/E 65.40 ÷ 46.85% |

| TTM revenue | $56.60M (Finviz) / $56.22M (StockAnalysis) | Finviz / StockAnalysis |

| TTM OCF | $13.65M (stats page) / $14.18M (cash flow statement) | StockAnalysis |

| TTM FCF | $11.58M | StockAnalysis (OCF minus $2.07M CapEx) |

| Quarter | Revenue | YoY growth | Net income | Adj. EBITDA |

|---|---|---|---|---|

| Q1 2025 | $11.5M | — | $1.1M | $1.3M |

| Q2 2025 | $12.6M | — | — | — |

| Q3 2025 | $13.5M | — | — | — |

| Q4 2025 | $14.5M | — | — | — |

| Q1 2026 | $15.5M | +34.63% YoY | $2.3M | $2.8M |

| FY2026E | $66–68M guidance | +27–30% guided | — | $12–14M guided |

| Metric | Finviz | StockAnalysis | Context |

|---|---|---|---|

| Trailing P/E | 65.40× | 67.72× | Elevated; net margin 15.58% on thin absolute earnings |

| Forward P/E | 41.60× | 42.52× | Consensus projects $0.30 EPS in FY2026 |

| P/S (TTM) | 10.36× | 10.55× | Standard for high-growth medical devices |

| EV/EBITDA | 72.21× | 81.16× | Discrepancy from different EBITDA definitions |

| P/B | 7.73× | 7.83× | Book value $75.80M ($1.99/share) |

| P/FCF | 45.68× | 51.21× | FCF $11.58M TTM |

| ROE | 12.55% | — | Reasonable for a recently profitable business |

| ROIC | 31.47% | — | High; reflects asset-light recurring revenue model |

| Gross margin | 75.51% | — | Stable for four consecutive quarters |

| Metric | Value (Mar 31, 2026) | Context |

|---|---|---|

| Cash & equivalents | $58.64M | Sufficient runway even at current growth CapEx |

| Total debt | $6.71M | Minimal; Debt/Equity 0.09× |

| Net cash | $51.93M ($1.36/share) | Strong position for a $593M company |

| OCF (TTM) | $13.65M–$14.18M | Positive for at least four consecutive quarters |

| FCF (TTM) | $11.58M | CapEx only $2.07M — asset-light model |

| Current ratio | 3.34× | Well above 1.0× |

| Quick ratio | 2.81× | — |

| Accumulated deficit | $88.52M | Historical losses from pre-profit years; not current risk |

| Long-term investments | $23.16M | Stakes in Neurolief, Axis, Stella MSOs |

| Risk | Severity | Impact path |

|---|---|---|

| Borderline TTM revenue growth | 🟡 Medium | StockAnalysis shows 29.37% — technically below the 30% hard filter by 63bps. Any deceleration in Q2 2026 (consensus $16.31M, +22% sequential from Q1) could push TTM below 30% on both platforms. The $66M–$68M FY2026 guidance implies back-half growth around 22–28%, a deceleration from H1's current pace. |

| Premium valuation with thin earnings base | 🔴 High | Trailing P/E 65–68×, EV/EBITDA 72–81×. BrainsWay earned $8.76M in net income on a TTM basis — $0.23/share. A single quarter of margin compression (as happened in Q1 2026, where EPS declined 16.7% YoY despite 35% revenue growth) compresses the P/E multiple disproportionately at these levels. |

| Single-customer concentration | 🔴 High | The 20-F for FY2025 discloses significant revenue concentration in a single large U.S. clinic customer. Exact percentage not disclosed publicly. Loss or contract renegotiation with that customer would "materially harm operations" per BrainsWay's own risk language. |

| Israeli geopolitical risk | 🟡 Medium | Operations and R&D headquartered in Jerusalem; manufacturing also in Israel. Geopolitical instability would disrupt production. Israeli government grants also restrict manufacturing outside Israel and technology transfer. Foreign private issuer structure (files 20-F, not 10-K) means less frequent and somewhat less detailed SEC disclosure. |

| PEG single-source limitation | 🟡 Medium | The entire PEG-based valuation case rests on Finviz's 46.85% five-year EPS growth projection for a company that earns $0.23/share on $56M TTM revenue. StockAnalysis cannot calculate or verify this figure. At $0.23 current EPS and a 65× trailing P/E, the stock is pricing in substantial earnings growth that has yet to materialize at scale. |

| Competitive pressure | 🟡 Medium | Neuronetics (NeuroStar) holds ~60% TMS market share. Emerging alternatives — esketamine (Spravato), psychedelic-assisted therapy protocols, digital therapeutics — compete for the same treatment-resistant depression patient population. BrainsWay settled a Lanham Act lawsuit with Neuronetics in January 2023, agreeing to stop using certain NeuroStar anxious depression efficacy claims in marketing materials. |

| IP concentration | 🟡 Medium | Core H-Coil patents are in-licensed from NIH and the Weizmann Institute. Termination of those licenses would effectively end Deep TMS commercialization. The U.S. government retains royalty-free worldwide usage rights for key foundational patents. |

| Firm | Analyst | Rating | Price target | Last action |

|---|---|---|---|---|

| H.C. Wainwright | Ram Selvaraju | Buy | $17.00 | May 26, 2026 (raised from $15) |

| Northland Securities | Carl Byrnes | Buy | $15.00 | Jan 22, 2026 (reiterated) |

| Ladenburg Thalmann | Jeffrey Cohen | Buy | $9.50 | Nov 12, 2025 (stale) |

| Catalyst | Expected timing | What to watch |

|---|---|---|

| FDA submission — Deep TMS for PTSD | Q2 2026 (imminent) | Filing confirmation would be a near-term positive; clearance timeline typically 6–12 months after submission |

| Q2 2026 earnings | ~August 2026 | Revenue vs. $16.31M consensus (+22% sequential), gross margin stability, RPO trajectory, installed base adds |

| Reimbursement decisions — accelerated protocol | Ongoing | Which payers follow Highmark (draft policy, Jan 2026) and Cigna (Feb 2026) in formalizing coverage for the SWIFT protocol; each new payer policy expands commercial addressable market |

| Adolescent MDD utilization ramp | H2 2026 | First full year of commercial availability for the 15–21 age group; whether clinic-level uptake matches the reimbursement expansion |

| Alcohol use disorder trial readout | 2026–2027 | NIH-backed RCT; positive data would set up a fifth FDA indication and the first substance-use indication beyond smoking |

Add more perspectives or context around this Post.